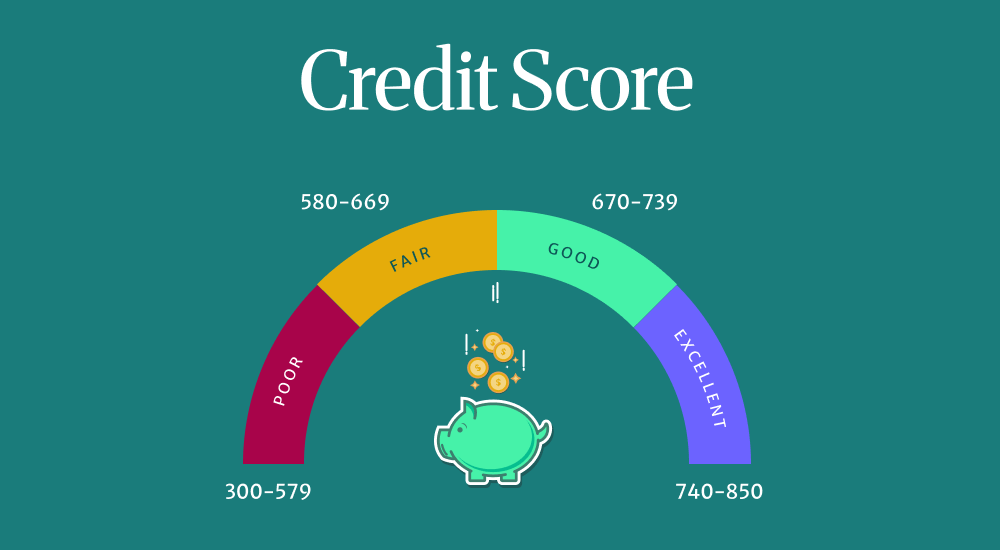

Credit Score: 5 Simple Ways to Boost a Low Credit Score

If your credit score is low, small, consistent actions can lift it up. These five steps are designed for people starting from the low-side who want fast, consistent improvement.

Wealthist

Financial insights for everyone

Five things you can do right now to get out of the credit basement

-

Pay every bill on time... even if it's just the minimum

Payment history is legit the single biggest factor in credit ratings. Set up autopay for at least the minimum payment due on credit cards and try to time your bills with your paychecks so missing payments doesn't tank your score.

We love this system: Setting up your calendar with your paydays so you always know when the next check is going to hit your account. Then you just plan all or some of your bills' autopay dates for the next day. That way, you're never worried about having enough, plus your payment history starts to look really good to credit bureaus.

-

Lower your credit card balances to under 30%

Credit cards all have a limit. Lots of them are around $5,000, but can go much lower or much higher depending on your salary, payment history, and a bunch of other factors.

Make some moves to get your credit card balances under 30% of your card’s limit. Going even lower is better. If you can, pay way more than the minimum to bring down your credit utilization faster. This can have a huge impact on your score.

-

Check your credit report for any errors and dispute them.

Get a credit reporting app. We love Credit Karma because it tracks your score and sends you alerts on your progress a lot. Using apps like this allow you to always see how your financial moves are impacting you in the eyes of credit cards, banks, and loan services.

-

Use a secured credit card or credit-builder loan responsibly.

If you can’t get a regular card, you could try a secured card or a retail credit card (like American Eagle, Macys, or Target). These cards help you learn about credit and establish your credit history.

Keep the card's balance very low and make sure you pay it off in full every month.

This is the riskiest way to build your credit if you've defaulted or missed payments in the past. Credit card debt is very easy to grow and very hard to shrink. If you can set this one on autopay and use it for one small bill every month, you might be ok to try this method.

-

Avoid applying for multiple new credit lines at once.

When you open a new card, finance a car, take out a loan, or even finance a new phone, companies usually check your credit. This inquiry into your financial life is called a hard-inquiry.

Hard inquiries might reduce your credit score temporarily, but you only need to worry about this temporarily. Focus on keeping your current accounts stable first; only apply when improvement makes approval likely.

Timeline & expectations

Small changes can produce visible results in a few months. But the noticeable improvement should happen within 6–12 months for things like lower balances and consistent, on-time payments. Removing old negatives can take a lot longer.

Helpful next steps

- Set autopay and calendar reminders for bill dates.

- Create a free Wealthist account to build your monthly budget.

- Check your credit often while building up your score (with Credit Karma or another tracking app).

Keep learning

Explore more basics articles. The more you know, the easier it is to build wealth.

Wealthist may earn commissions from products or services on this page at no extra cost to you. We recommend products we trust, but do your own research before purchasing or downloading anything new. If you'd like to learn more, check out our terms of use and privacy policy.

Expert guidance

Ready to talk to a real advisor?

Households that worked with a financial advisor for 15+ years accumulated 290% more assets than those who didn't.*

Connect with an expert →No spam. No obligation.